Have you ever wondered why your credit score is so important? Don’t worry, I’ll explain it in simple terms. Your credit score is the financial report card that shows the lenders how good you are with money. Your credit score makes things easier or harder when it comes to buying a car, renting an apartment, and even getting a job. Let’s discuss why it’s important and how it affects your money.

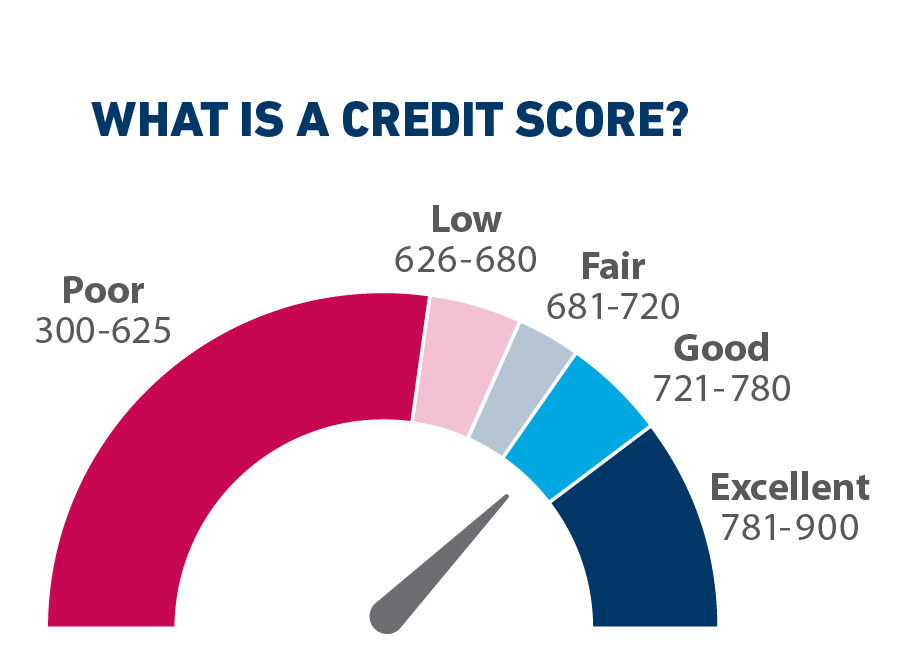

What is a Credit Score?

Consider your credit score to be your financial reputation. It is a number between 300 and 850 that gives lenders an idea of how likely you are to repay borrowed money. A high score means you’re trustworthy, and a low score makes lenders jittery.

For instance, a teacher, Emily, has a credit score of 780. Since her score is high, she receives a low-interest loan to purchase her first home. Jake’s credit score of 600 results in his being denied the same loan or receiving the same loan but at a higher interest rate. Look at how a good credit score saves you money and headaches!

Why Does Your Credit Score Matter?

Your credit score affects your money in many ways. Here’s how:

1. Getting Loans

Whenever you want to take a loan for a car, a house, or even something small, consider your credit score. The better the score, the more likely they will say yes and give you better terms.

For example, Lisa wants to purchase a car. With her credit score of 820, she gets a loan with an interest rate of 3%, while her friend Alex gets a loan with an interest rate of 9% because his credit score is 650. His credit score is very low; therefore, he pays significantly more for the same car.

2. Lower Interest Rates

This is the extra cash you pay to borrow money. A high credit score gets you lower interest rates, which means you save money.

For instance, Sarah borrows $10,000 at 5% interest to fix her house. John, who receives the identical loan at 12% due to his lower score, pays more than she does overall.

3. Renting a Place

Homeowners often look at your credit score when you look to rent a home or apartment. They use it to figure out your chances of making your rent payments on time. If your score is high, they’ll feel more confident about renting to you. However, if your score is low, you can get rejected, require a co-signer, or have to pay a larger security deposit.

Anna, for instance, wants to rent her first apartment. Her request is immediately approved with a credit score of 750, and she is just required to pay the normal deposit. Sam needs his dad to co-sign the lease and pay an additional month’s rent in advance because he has a 580 credit score. This points out how having a high credit score can make renting much easier and less stressful.

4. Getting a Job

Did you know that some employers check your credit history before offering you a job? They do not see your actual score but rather view your credit report for items such as late payments, high debt, or accounts in collections. This is quite common in jobs that require handling money or sensitive information.

For instance, companies may check your credit report to determine your level of financial responsibility if you’re looking for a job as an accountant or bank teller. Meet Tom, who has a history of late payments and unpaid debts. The company might worry that Tom’s financial problems could affect how he handles work or put him under stress. On the other hand, Lisa, who has no late payments and no big debts, looks dependable and gets the job more easily. This shows how keeping your credit in good shape can make a big difference when job hunting.

But it does not mean you won’t obtain the job if your credit isn’t flawless. A strong credit history enhances your impression, just like bringing a well-formatted resume to an interview.

How to Make Your Credit Score Better

If your credit score isn’t great, don’t worry. You can fix it. Here’s how:

- Pay Bills on Time: On-time bill payment improves your credit score. To keep on track, apply autopay or set reminders.

- Use Less Credit: Try to keep your credit limit usage to a minimum. Let’s keep it below 30%.

- Verify for Errors: Credit reports may sometimes contain mistakes. Review yours and deal with any issues.

- Avoid Applying for Too Much Credit: Your credit score might drop slightly each time you apply for credit. Apply only when truly necessary.

- Keep Old Credit Cards Open: It’s better to have a longer credit history. Keeping an old card open can be beneficial even if you don’t use it.

To discover about Why Hiring a Professional Tax Filer, read 6 Reasons Why Hiring a Professional Tax Filer Could Save You Time and Money

Final Thoughts

Your credit score is more than a number. It’s a tool that can help you meet your goals and save money. A high credit score is important whether you want to launch a business, purchase a home, or simply feel confident about your financial situation. Get started raising your score right now, and see how it helps you get more opportunities.

Concerned about your credit? Let’s talk! My motive is to assist you in taking charge of your financial future.

To discover about Single Mom’s Tax Refund, read Maximizing Your Tax Refund: A Single Mom’s Cheat Sheet

Frequently Asked Questions (FAQ)

- What is a good credit score?

A good credit score is usually 700 or higher. The higher your score, the easier it is to get loans and lower interest rates.

- How can I check my credit score?

You can check your credit score for free using online services like Credit Karma or your bank’s app. You’re also entitled to a free credit report once a year from AnnualCreditReport.com.

- Will checking my credit score lower it?

No, checking your credit score is a “soft inquiry” and doesn’t affect your score. However, when lenders check it, it’s called a “hard inquiry,” and that can lower your score slightly.

To discover more about tax filing software options, read Top 5 Tax Filing Software Options: Which One is Right for You?