One of the best financial decisions you can make is raising your credit score. Why? Because you can eventually save a ton of money by qualifying for loans with cheaper interest rates if you have a higher credit score. Let’s explore some simple, practical strategies for raising your credit score.

What is a Credit Score and Why Does it Matter?

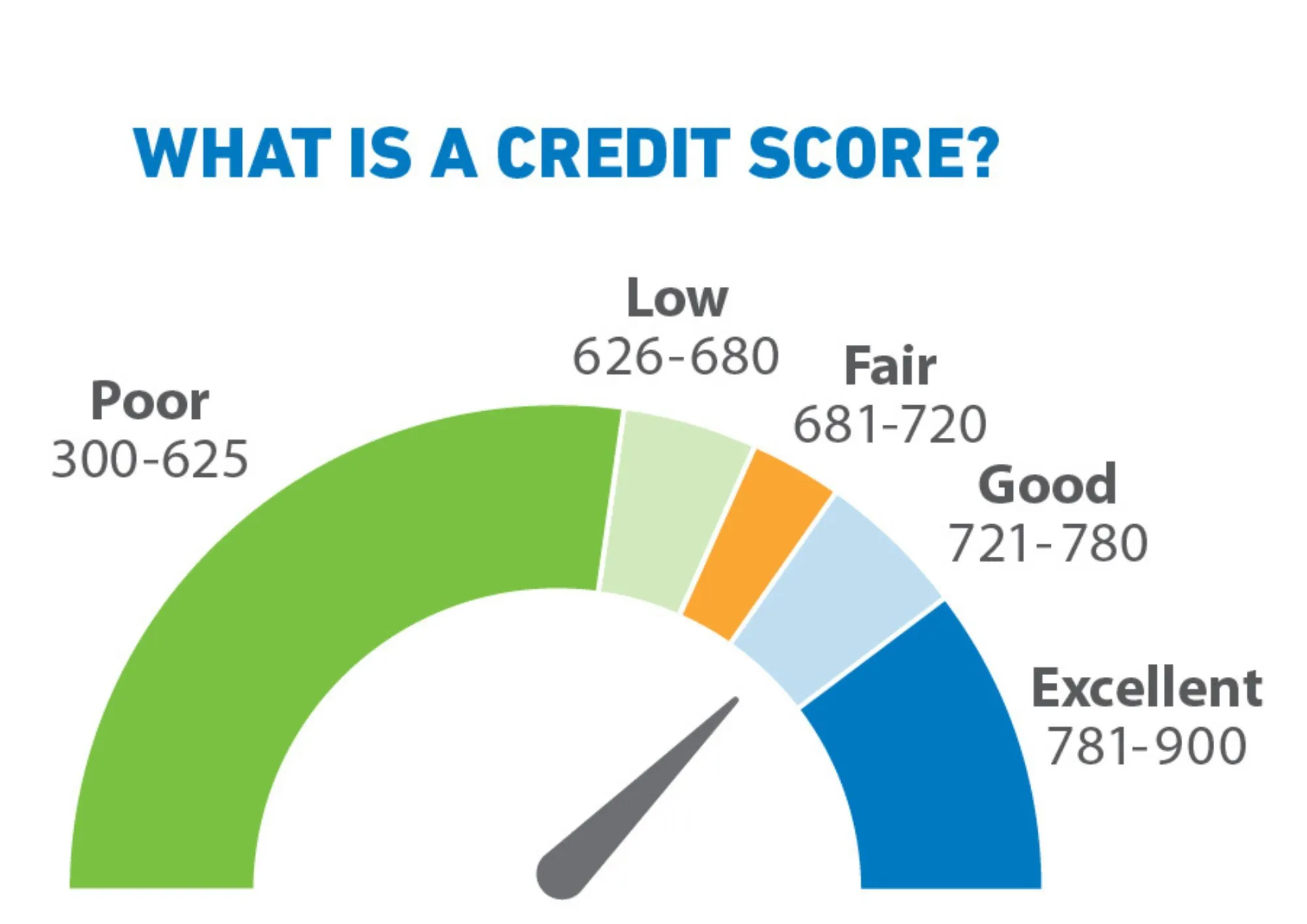

Let’s quickly review the meaning of a credit score before moving on to the tips.

Your credit score is a number that indicates your level of financial reliability. It falls between 300 and 850. A higher score gives lenders more confidence to provide you with a loan because it indicates that you manage your debt well.

You not only get approved for loans with a higher score, but you also obtain better rates. For example, a person with a credit score of 780 would be eligible for a loan with 3% interest, whereas a person with a score of 620 might be forced to pay 9%. There is a huge difference!

Tips to Improve Your Credit Score

1. Pay Your Bills on Time

This is the credit score golden rule. More than anything else, late payments lower your credit score. Make sure you never forget a deadline by using autopay or setting reminders.

So, for example, let’s suppose Emily has a credit card statement that is due on the 15th. Her credit score might suffer a lot if she forgets and pays it on the 20th. However, she guarantees that her bill is always paid on time by setting autopay.

2. Keep Your Credit Utilization Low

The amount that you are using of your available credit is known as credit usage. Aim for less than 30%. For example, don’t spend more than $300 if your credit limit is $1,000.

Advice: You can contact your credit card company to raise your limit or pay off debt if you’re using too much credit.

3. Check Your Credit Report for Mistakes

Errors in credit records can sometimes lower your score. Every year, websites such as TransUnion.com offer a free credit report. If you see mistakes, report them and have them corrected.

For example, Jake found an unauthorized loan on his credit record. His credit score increased by 50 points after the credit agency erased it after he reported it.

4. Don’t Apply for Too Much Credit at Once

A “hard inquiry” is made each time you ask for credit, and it may result in a minor drop in your score. Avoid applying for several loans or credit cards at once.

Tip: Apply only when necessary.

5. Keep Old Credit Cards Open

Your credit score is heavily affected by the duration of your credit history. Even if you don’t use your previous credit cards frequently, keeping them open allows you to build up a longer credit history, which raises your credit score.

For example, even if Sarah rarely uses her first college credit card, its lengthy history proves that she is a reliable borrower, which continues to raise her credit score.

So, your credit history should be as long as possible. Keeping an old card open improves your score even if you don’t use it.

6. Diversify Your Credit Mix

Your score can be raised by having a variety of credit, such as a mortgage, auto loan, or credit card. However, you don’t need to take on debt to improve your credit mix.

Tips: Concentrate on maintaining your current accounts.

How Long Does It Take to See Results?

It takes time to raise your credit score, but in as little as a few months, little adjustments can have a major impact. Your score could be swiftly raised, for example, by settling a credit card debt or correcting a mistake on your credit record. More major adjustments, such as establishing a track record of timely payments, could take a year or longer.

The Benefits of Raising Your Credit Score

Getting approval for loans is not the only benefit of having a higher credit score. It also means:

- lowered interest rates, which result in financial savings throughout your loans.

- faster and simpler approval for home or apartment rentals.

- reduced utility deposits and favourable conditions for insurance plans.

Imagine it a financial improvement that simplifies and lowers the cost of living!

To discover more about Credit Score Affects, read How Your Credit Score Affects Your Financial Health

Final Thoughts

Although boosting your credit score may seem difficult, it is completely possible if you follow the correct procedures. Start by verifying your credit report for mistakes, paying your bills on time, and using your credit sensibly. Over time, these minor acts might have a major effect.

Are you curious about how your credit score affects your financial health? Check out our credit score blog. You’ll be closer to better lending rates and financial freedom the earlier you begin!

To discover more about Head of Household Tax, read Head of Household: An Easy Guide to Saving on Taxes

Frequently Asked Questions(FAQ)

1. Will my credit score increase immediately if I pay off all of my debt?

Debt repayment can be positive, particularly if it reduces the amount of credit you use. However, payment history, credit age, and credit mix can affect your score.

2. How is my credit score affected by late payments?

Your score can be severely impacted by late payments, particularly if they are more than 30 days past due. The secret to raising your score is to always make your payments on time.

3. Is having too many credit cards an unfortunate thing?

If you use your cards sensibly, having several isn’t a bad thing. However, your score might drop if you apply for too many cards at once.

To discover more about American Tax Savvy, read American Tax Savvy: Maximize Your Refund, Deduct Your Bill